Business Valuation Key Man Discount

Business Valuation How Investors Determine The Value Of Your Business Entrepreneur S Toolkit

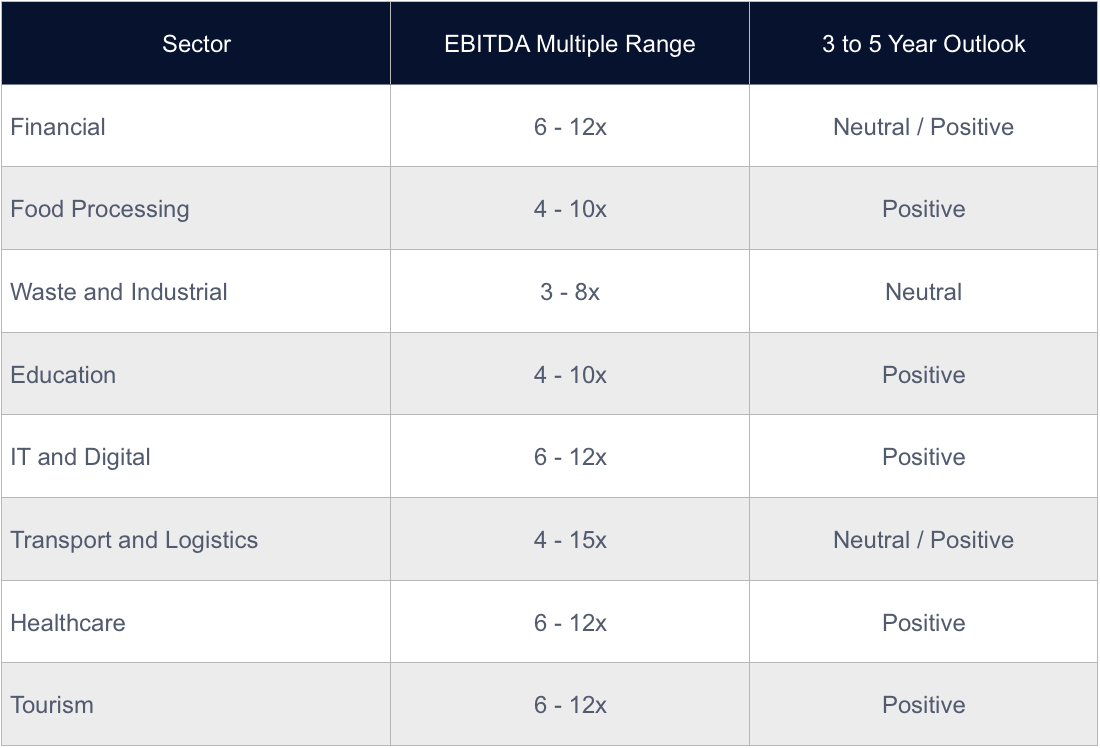

Business Valuation Multiples By Industry Nash Advisory

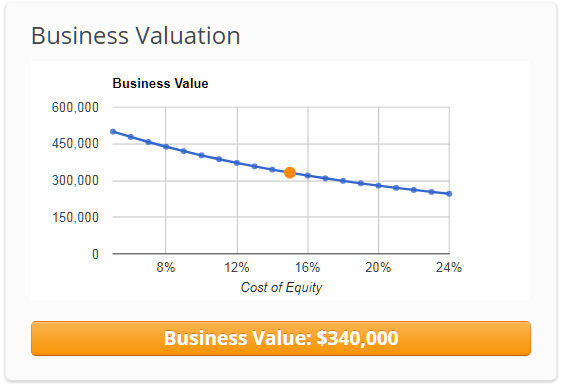

Business Valuation Calculator Exitadviser

Your Financial Dashboard Virtual Accounting Insights And Analysis Business Intelligence Dashboard Business Intelligence Financial Dashboard

Company Valuation Powerpoint Presentation Slides Graphics Presentation Background For Powerpoint Ppt Designs Slide Designs

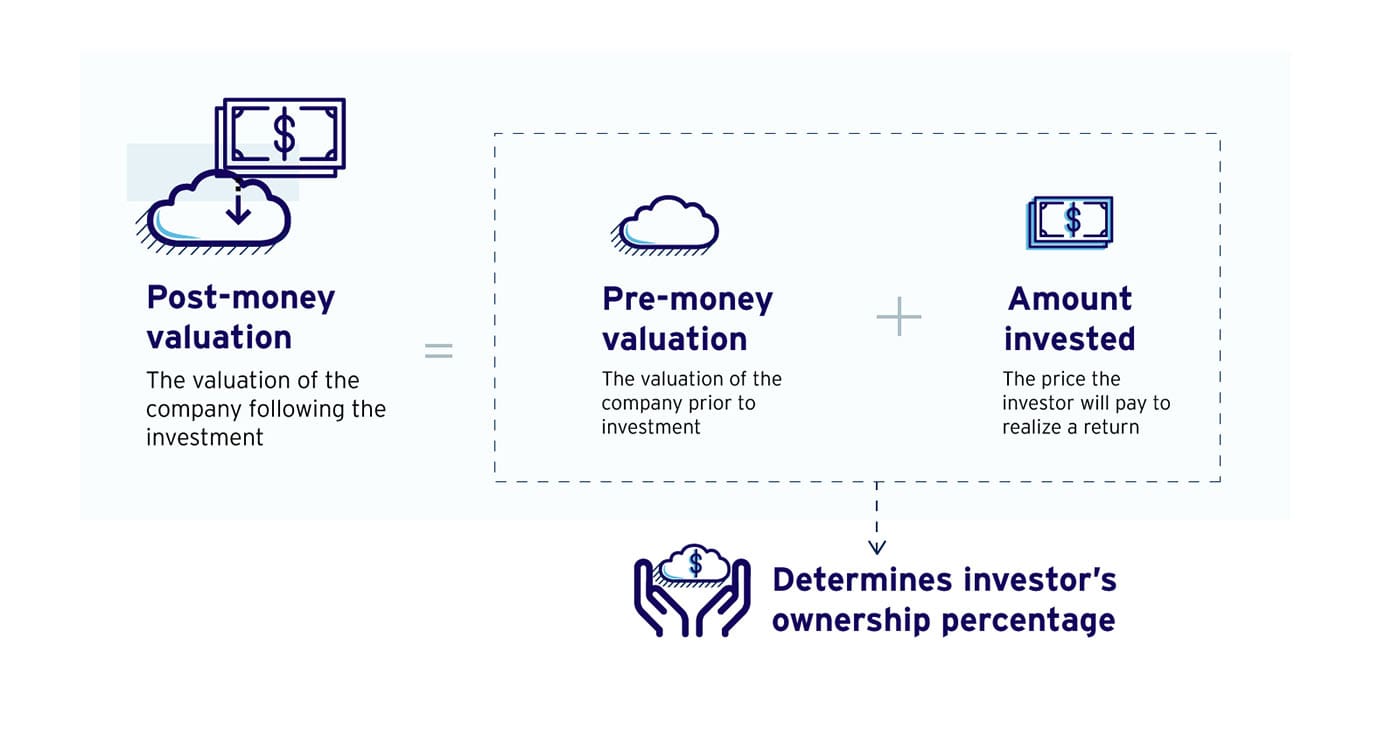

Venture Capital Method For Company Valuation Venionaire Capital

When valuing closely held companies for marital dissolu.

Business valuation key man discount. The definition of a key person discount is an. An important consideration called a key man discount was presented at court in relation to the date of value to pinpoint the fair value for the business. The key for successfully utilizing discounts and or premiums is to truly understand the ownership characteristics and attributes of the subject equity interest and the third party supporting base data.

Having a key person as a large revenue generator would likely materially affect the financial position of the business. According to the international glossary of business valuation terms a key man discount is. Under estimate the discount rates.

The analysis above provided me with the foundation to discount the value of the lobbying business based on the importance of the key person owner. Quantifying the discount is a challenge because unlike marketability and minority discounts there s little empirical support for across the board key person discounts in business valuations. An amount or percentage deducted from the value of an ownership interest to reflect the reduction in.

Instead of taking a separate discrete discount at the entity level some experts incorporate a key person discount into their valuation methodology. An amount or percentage deducted from the value of an ownership interest to reflect the. Mary ann lerch 1992 discount for key man loss.

This key person may be a revenue generator possess technical. Practice pointers revenue ruling 59 60 sets forth the premise that valuation of closely held business interests is. Consequently the buyer of the business will have to factor in an illiquidity discount to estimate the value of the business.

A key person or thin management discount would be appropriate in the valuation of a closely held company to the extent that an owner or employee who would be difficult to replace is responsible for a significant or material portion of the business such as sales or profits. Although the approach for implementing the discount and subjectively assess its magnitude had to be determined an objective basis for the existence of the discount had been established. For example under the income approach a valuation expert might adjust the discount rate capitalization rate or projected cash flows to reflect key person risks.

Pin On Business Valuation

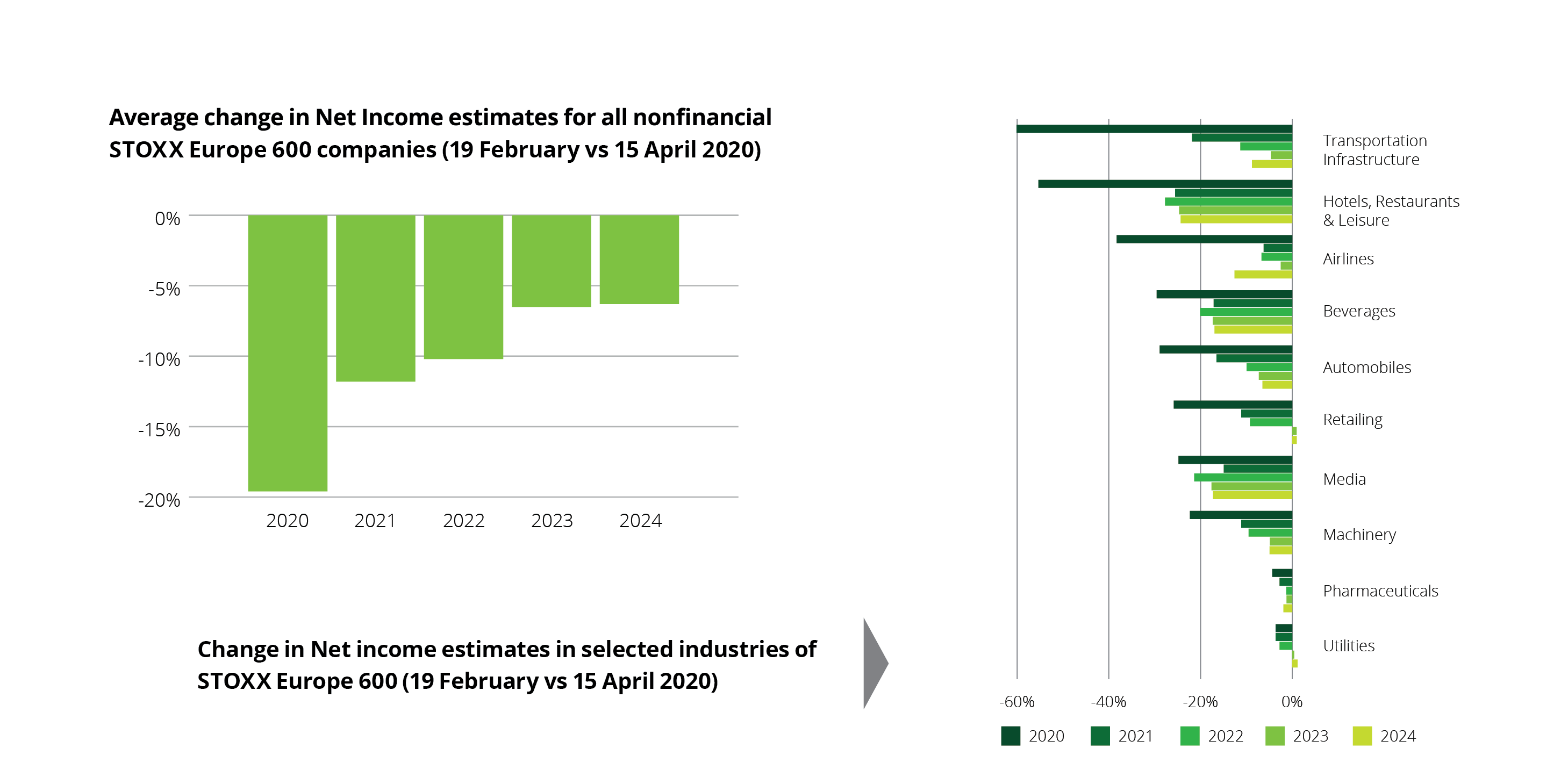

Impact Of Covid 19 On Business Valuation In Europe

Business Valuation Powerpoint Presentation Slides Presentation Graphics Presentation Powerpoint Example Slide Templates

Infographic The Highest Valued Startups In The World In 2020 Startup Company Startup Infographic Startup Presentation

Career Is Choosing It S All About Youth Difficult Now Choosing A Career Career Priorities

Business Valuation Letter Sample Manswikstromse With Valuation Letter Template In 2020 Scholarship Thank You Letter Thank You Letter Examples Thank You Letter Sample

Dividend Growth Model Calculator Free Excel Valuation Model Dividend Investing Dividend Investment Tools

An Overview Of M A Valuation Methods Midaxo

Mapping Infographic Assessment Review Human Resources Map

Business Valuation Valuation Services

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcr3xngdwi5cl5z95gk3srq1yxagbc1tu5xbfa Usqp Cau

Startup Valuation Methods Six Tips For Helping Ceos Maximize Valuations Business Valuation Startup Advice Small Business Advice