Opportunity Zone Business Qualifications

What To Know About The Tax Benefits Of An Opportunity Zone Bader Martin

Second Wave Of Opportunity Zone Guidance Addresses Many Key Issues Leaves Open Questions For Future Guidance Insights Skadden Arps Slate Meagher Flom Llp

Qualified Opportunity Zones What Investors Should Know The Private Bank

Https Www Irs Gov Pub Newsroom Tcja Training Opportunity Zones Qualfied Opportunity Funds Pdf

How It Works Division Of Small Business State Of Delaware

Opportunity Zones Colorado Office Of Economic Development International Trade

As part of the tax reconciliation act of 2017 us congress enacted an incentive to spur economic development and job creation in designated distressed communities or qualified opportunity zones qoz.

Opportunity zone business qualifications. In addition the business needs to satisfy the following requirements. Applying these two definitions together means that during the entire time in which the qof or qoz business owns or leases tangible property at least 63 of the use of that tangible property must be in a qoz. Opportunity zone funds must hold at least 90 percent of their assets in qualified opportunity zone property such as an opportunity zone business.

The qualifications as qualified opportunity zone stock qualified opportunity zone partnership interest and qualified opportunity zone business property encompass investments in new or substantially improved tangible property including commercial buildings equipment and multi family complexes with a common requirement that such investments must be made in qualified opportunity zones. The new guidance clears this large hurdle by creating four distinct tests that can be used to qualify a business under the new 50 test. Thus during at least 90 percent of the time in which the qof or qoz business holds or leases the tangible property at least 70 percent of the use of that property by the qof or qoz business must be in a qoz.

On february 27 2018 the cdfi fund posted an update to their safe harbor eligibility data on their opportunity zones information resource it results in an additional 168 low income communities an additional 1 007 additional eligible contiguous tracts and 72 formerly eligible contiguous tracts that are no longer deemed eligible. Exactly 70 or more of the tangible property owned or leased by the business must be qualified opportunity zone business property qozbp located in a qoz. For a business to qualify the tangible property owned or leased by the business needs to be qualified opportunity zone business property i e acquired after december 31 2017 and meet the original use or substantial improvement test.

This seminar addressed the technical challenges and practical strategies for setting up a qualified opportunity zone business qoz business before the end of 2018. And proposed regulations currently specify that for each taxable year at least 50 percent of the gross income of a qualified opportunity zone business must be derived from the active conduct of a. Total hours worked by employees and independent contractors.

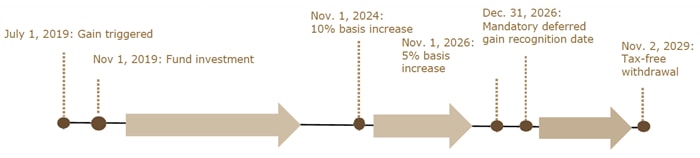

This allows the gain to be deferred until 2026 when it is recognized without regard to whether the qof interest is sold. The 2017 tcja added a new deferral mechanism for capital gains realized from any source. Ii a substantial portion of the intangible property of such entity.

Qozbp is tangible property acquired by a qozb after december 31 2017 and either the original use of such property needs to start with the qualified opportunity fund investment or the fund investment must substantially improve the property. The taxpayer can realize a capital gain and then reinvest only the amount of the gain in a qualified opportunity fund qof within 180 days of the realization event.

Opportunity Zones Are Open For Business 5 Key Features Of The New Guidance

Opportunity Zones New

Federal Opportunity Zones

Https Www Irs Gov Pub Irs Pdf I8996 Pdf

Https Www Davispolk Com Files 2019 07 02 Proposed Regulations Likely To Stimulate Investment In Qualified Opportunity Zones Pdf

Opportunity Zone Fund Directory Ncsha

What Are Qualified Opportunity Funds Opportunitydb

Primer On Opportunity Zones And Qualified Opportunity Funds Eligibility Requirements And Tax Considerations

Can An Llc Qualify As An Opportunity Fund Opportunity Zones Q A

How Your Nonprofit Can Get Involved In Opportunity Zones Wipfli

-(1).jpg.aspx)

Second Set Of Opportunity Zone Guidance Bdo Insights

Qualified Opportunity Zones Proceed With Caution

An Overview Of Business Incentives